Nutmeg State FCU Deposit Protections

A message from our CEO John Holt

Understandably, the recent news regarding the collapse of Silicon Valley Bank & Signature Bank has caused significant uncertainty & concern within the banking sector. At Nutmeg State we are committed to keeping your deposits safe and protected. Below you will find additional information on how Nutmeg State Financial Credit Union works to properly secure your accounts. Should you need assistance or have additional questions please contact us by email at memberexperience@nutmegstatefcu.org or by phone at 860.513.5000.

John Holt, CEO

Nutmeg State Financial Credit Union’s first priority is our members’ financial success and security.

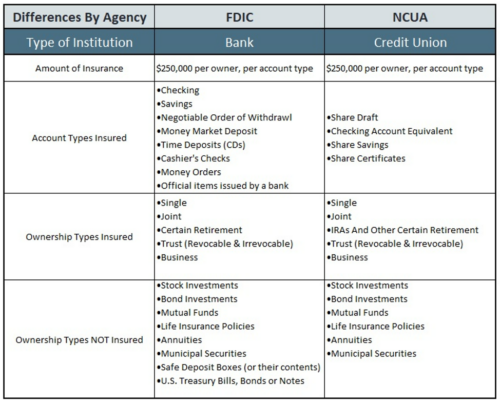

Nutmeg State Financial Credit Union is a state chartered, federally insured credit union. Deposits are insured by the NCUA’s National Credit Union Share Insurance Fund up to $250,000 per share deposit owner for each account ownership category. For additional information on insurance limits and how to calculate your insurance coverage use the links provided below.

Facts that make Nutmeg State & other CT credit unions reliable and safe for your deposits

- Nutmeg State is in good financial condition with a Net Worth Ratio nearly double the amount of the the minimum/required Net Worth Ratio of 7%.

- Credit Unions are member-owned cooperatives. As a result of being a member-owned cooperative, credit unions are much less risky with investment options.

- Banks, typically, rely on borrowed money to sustain operations. Additionally, banks invest heavily into securities markets. Credit unions are restricted in how much and what types of investments they may use.

- Credit union members have never lost a penny of insured savings at a federally insured credit union, and our industry’s deposit insurance fund has the backing of the full faith and credit of the U.S. government.

- All Connecticut credit unions are regularly examined by multiple financial regulators to ensure proper management and maintain the safety and soundness of members’ money.

- The credit union system remains well-capitalized and on a solid footing. The National Credit Union Administration continues to monitor credit union performance through both the examination process and offsite monitoring, and it will continue to do so into the future.

With coverage provided by both the FDIC and NCUA, you can rest assured that your money is protected (up to set limits) by the federal government.

The NCUA insurance covers many common deposit accounts but doesn’t insure investment accounts. Here are the following types of accounts that are ineligible for coverage:

-

- Stock Investments

- Bond Investments

- Mutual Funds

- Crypto Assets

- Life Insurance Policies

- Annuities

- Municipal Securities

- Safe Deposit Boxes (or their contents)

- U.S. Treasury Bills, Bonds or Notes (these investments are backed by the full faith and credit of the U.S government).

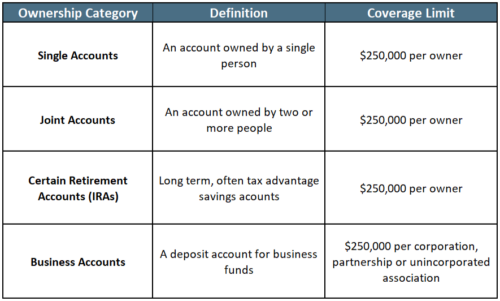

Open joint accounts: Maxed out your single account coverage? By opening a joint account with one or more people who you trust, you can expand your insurance coverage beyond $250,000.

Open single accounts within a family: Every bank account is insured for $250,000. If you have funds as a family that exceed that and you’d like to keep the money available in deposit accounts, have family members open their own accounts rather than keeping money in one account.

Establish trusts with beneficiaries: Open an account associated with a living trust and choose up to five beneficiaries –– that’s five times the amount of coverage.

Open accounts at various Institutions: Each depositor is insured per bank, per ownership category. You can open accounts at the same bank, each under a different ownership category, or open a new account at more than one bank.

Open a retirement account: Certain retirement accounts are insured by the FDIC/ NCUA. If you’ve exceeded your limit in other ownership categories, and are saving for retirement anyway, make sure you’re taking advantage of retirement accounts. Beneficiaries will not get you more coverage.